Published on 14th March 2026

The UK economy’s performance in January should not have come as such a surprise to numerous ‘economic analysts’.

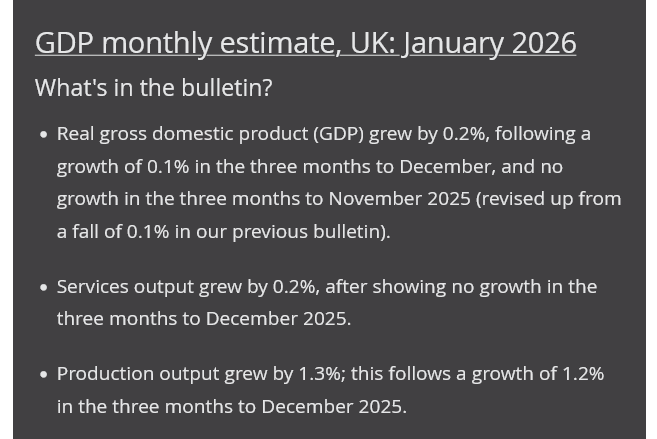

November GDP was boosted by accountancy advice, as people tried to predict and mitigate the measures in Labour’s November 2025 Budget.

December GDP will have ticked up thanks to Christmas.

Now we are back in stable state: stagnation of the headline figure.

Underneath that the news is even worse, as there are numerous factors supporting statistical GDP which betoken wealth destruction and manipulation – and I am not referring to the Office of National Statistics being headed by a Labour Party hack, although that helps (the government).

Strip out these factors and there is a private sector economy in deep trouble.

Elements – like social work – are counted within GDP although they are an expenditure of wealth, not a creation of it.

The cost-of-compliance with government regulations – like a subscription to MTD compliance software – are impositions on business and diminish private sector wealth, without reducing government spending or taxes. A new MTD software subscription – such as for the 800,000 businesses that are compelled to buy this year – expands GDP. This is a template for regulation driving GDP growth, but not in a good way.

The expansion in the government’s day-to-day spending is reflected as additional GDP – for example as rising sales of hospital services – but it is financed by borrowing, and therefore has a deflationary, wealth-reducing impact in the medium term, whilst providing a sugar rush of growth in the short term.

The expansion in spending that is state-directed but nominally carried out by private sector companies – such as on Net Zero – is also 100% debt-funded and triggers a shorter-term sugar rush of additional GDP, even more so as the target date for decarbonisation is brought closer.

In this case the debt counts neither as government debt nor as Public Private Partnership debt. It bypasses the provisions of the government’s Green Book and all the supposed controls trotted out by the government in its papers accompanying the November 2025 budget on ‘Balance sheet framework’ and ‘Managing Government’s Implicit Liabilities’. An orgy of spending in the short term will be followed by a colossal financial hangover.

But we are in the ‘short term’, all those elements are feeding into GDP already, and yet GDP is stagnant. That points to a private sector economy which is in a deep recession.