Published on 4th June 2026

Introduction

The John Lewis pension scheme was hit with major losses in 2022. This was largely due to its exposure to Liability-driven investments, or LDIs. Covering the losses sucked in all of its listed investments, leaving the fund essentially as a betting vehicle – will the residual assets return the discount rate at which the fund’s future liabilities are discounted?

John Lewis financial reporting dates

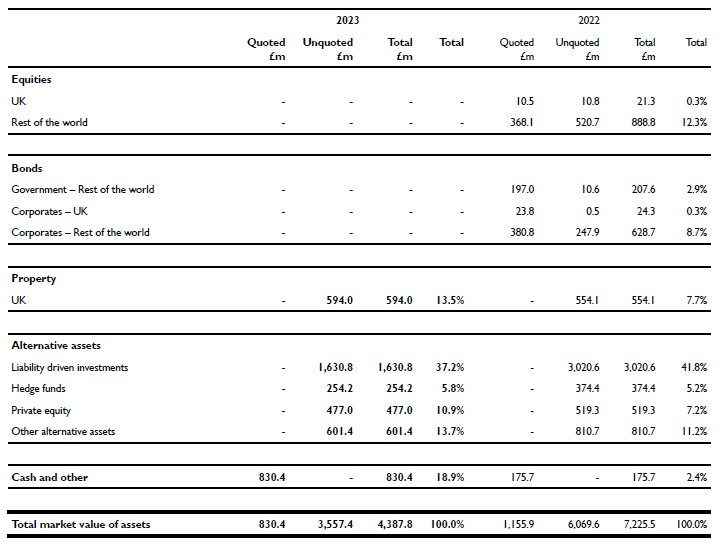

The picture to the side, which contains the figures quoted in the blog, is taken from the 2023 John Lewis (JLP) annual report. The JLP reporting date is curiously the end of January, such that the figures in the 2023 annual report are akin to those in a 2022 annual report issued on the more normal date of 31st December.

Status at the start of 2022

At the start of its 2022/3 financial year, on 1st February 2022, John Lewis’ corporate pension fund had a value of £7.2 billion. £3.0 billion of that was in derivative contracts called Liability-driven investments, or LDIs, to which banks were the counterparties.

An unspecified portion of the cash of £175 million will have been pledged as margin to the banks to protect them against a fall in the value of these LDIs.

The reference asset for the LDIs was UK government bonds, or ‘gilts’, but the reference formulae used were many and various, usually including clauses that magnified the loss on the LDI compared to the loss on a straightforward holding of gilts in the same amount (a characteristic known as leverage).

Status at the end of 2022

By the end of the 2022/3 financial year the fund had fallen in value by £2.8 billion to £4.4 billion, or by 39%. This was due to the general rise in interest rates, and to the particular, spectacular fall in the value of gilts around the Mini-Budget in September 2022. The spectacular fall in value of gilts was magnified through the reference formulae to produce even larger losses on the LDIs.

At the end of the financial year on 31st January 2023, the fund owned £1.6 billion of LDIs, the same amount of property it had owned a year before, and now £830 million of cash.

Cash margin pledged to banks

The cash amount reflected the increased margin that the bank counterparties to the LDIs now required. It remained unclear how much of the cash was hypothecated in this way, but for purposes of illustration let us assume that 50% of it was: £87.5 million pledged to banks as margin in February 2022 had risen to £415 million in January 2023, but on a portfolio of £1.6 billion compared to one of £3.0 billion.

The margin percentage had escalated from 2.9% of contract value (87.5/3,000) to 25.9% (415/1,600).

How the increases in volatility and the fall in gilt prices stoked one another

This rapid escalation in the margin amount called for by the banks is what caused the firesale of both gilts and other assets in September 2022. The margin call rose because of rising interest rates and increasing volatility. These fed one another in a merry-go-round: margin calls rose, then gilt prices fell as parties sold off their stock to meet the margin calls.

The volatility of the reference asset was pushed up by these sales, at the same time as the intrinsic value of the reference asset was being pushed farther down. These gyrations were captured by the banks’ financial models that calculated the margin, margin calls rose….and round we go again, and even more quickly.

Sale of all listed and liquid assets

It is clear that the John Lewis fund had to sell all of its listed and liquid assets to meet these margin calls: it ended up owning no equities or bonds at all. Its assets are all illiquid – alternative assets and some property – with the exception of whatever portion of the cash is not hypothecated.

Silver lining to this disaster

The black cloud had a silver lining: higher interest rates permitted that the fund’s liabilities could be discounted at an elevated interest rate. The Net Present Value of the liabilities then magically turned out to have fallen by even more than the much-depleted value of the assets.

It could be argued that the LDIs had done their job – but only by a financial apologist reminiscent of a surgeon claiming to have saved the life of a patient who came in for a spleen removal by taking out one kidney and half the liver as well.

Conclusions

The fund performed disastrously badly in 2022 but remained solvent. This solvency is entirely dependent on the realism of the discount rate.

The discount rate employed is the yield on a AA-rated corporate bond of the same duration as the fund’s liabilities, which is 40-50 years.

There are no AA-rated corporate bonds at that maturity in UK pounds, at least not senior, unsecured ones. The discount rate has been extrapolated from the ‘long gilt’ yield at 30 years, with a margin added for the credit risk premium appropriate to lending to a corporate instead of sticking with the risk-free investment in gilts.

The fund assets will meet its liabilities if the fund’s assets, including the LDIs, yield the discount rate on a compounded basis over the coming 40-50 years. Can that be insured through Bet365? This is precisely what LDIs were meant to insure, and the reader can make up their own mind whether they have been successful.