Published on 20 July 2021

What are HM Treasury and the EU playing at? Their dispute rumbles on over whether the Brexit divorce bill is the EU’s estimate of £41bn or HM Treasury’s (or rather the Office for Budget Responsibility’s) of £35-39bn.

The discussion feels phoney. The quoted amounts cannot include all the items that the treaty states are in-scope of the calculation, and neither side can know how many of the items will default or fail such as to give rise to a cash claim at some future point.

I am baffled as to why both sides continue with this, unless it is a deliberate ploy to blow smoke in people’s eyes (our eyes).

As I have done before so as to contribute to Centre for Brexit Policy papers, I have looked again at the UK/EU agreement of 2019 as the reference point (and not the 2020 Act of Parliament which adopted it):

https://ec.europa.eu/info/relations-united-kingdom/eu-uk-withdrawal-agreement_en

Some ingredients are not yet known because of the carryover provision (Article 140.1); the cash payments in respect of others cannot be known until the underlying programmes and activities either default or are closed.

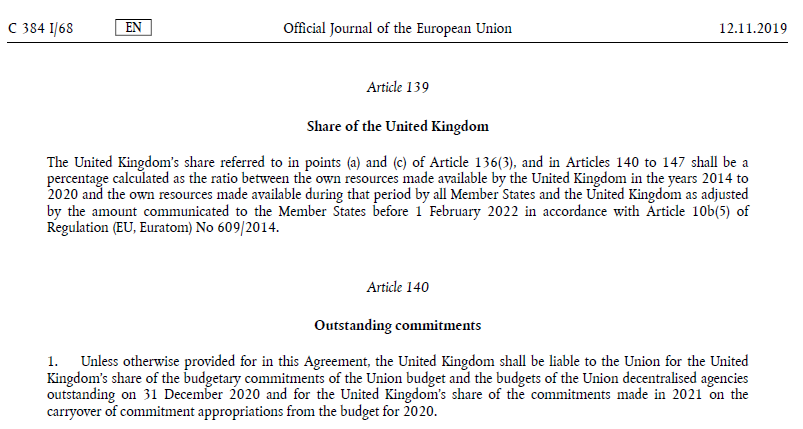

One of these is the European Financial Stability Mechanism, where the final repayments are only due in 2042: each of Ireland and Portugal must repay EUR1.5bn on 9 January 2042, but if one or other or both fail to repay, the EU’s bonds must still be repaid and the shortfall is marked against the UK’s card. As it stands, the UK would have to pay +/-12% of the EUR3bn, or EUR360 million.

Another is the European Investment Bank’s (EIB) loan programme outside the EU, where the EIB has a first-loss guarantee from the EU. These loans can be drawn over several years so if the EIB agreed to lend Algeria EUR20bn in 2019 with a drawing period of 4 years, it can still be drawn in 2022 and all of it will go against the UK’s card – because the commitment was made within the 2014-20 Multiannual Financial Framework (MFF) period and thus gets counted against the EU’s guarantee issued in that MFF.

More worrying is the amount through the InvestEU programme, in which the European Investment Fund (EIF) has a prominent role alongside its parent, the EIB. EIB/EIF enjoy a first-loss guarantee from the EU for their InvestEU transactions. EIB makes loans that presumably do have an end date, even if they are subordinated to senior lenders and involve a high credit risk. The EIF has undertaken transactions that either have a much longer end-date because they are guarantees of long-dated subordinated loans, or they have no end-date at all. All of these EIF operations have a very high credit risk.

Art 118.3.b includes any “financing, guarantee, investment” of the EIB and specifically of the EIF until the operation itself runs off. This means that any losses by the EIF on its guarantees or “equity commitments” in InvestEU are part of the UK’s calculation. We do not know the run-off profile of the EIF’s guarantees but the EIF’s “equity commitments” have no natural end-date. If the “equity commitments” are called, the EIF will own shares that qualify as an “investment”. Shares have no end-date so the UK is on the hook for the duration.

Art 138.1 confirms that the UK is on the hook with regard to all programmes and activities committed within the 2014-20 MFF and previous MFFs: that means that if a ceiling has been agreed for a programme during a qualifying MFF but a portion remains undrawn, the undrawn portion can be drawn and will qualify within the UK’s calculation.

Art 140.1 is the one that puts the UK on the hook for any new programmes and activities committed up to the end of 2021 under the carryover provision of the 2014/20 MFF, so we do not yet have a final listing of what operations are even within scope.

Art 140.2 says that a list should have been produced as of 31 March 2021 stating what was in-scope at that time – and this should have included the undrawn portions of committed programmes and activities and any new ones committed within the 2014-20 MFF under the carryover up to 31 March 2021.

Art 140.3 says that this list will be refreshed every year, so the one of 31 March 2022 must then contain all programmes and activities committed under the carryover which expires on 31 December 2021.

Art 140.5 allows the UK to request the ability to make a single determining payment on 31 December 2028. The wording of this Article alone is a dead giveaway that no-one can know the final figure now.

At least the the UK’s share would be about 12% of any loss (Art 139 limits our share of any such loss to the UK’s share of the 2014-20 MFF divided by the total 2014-20 MFF) and not potentially the full amount: member states’ guarantee of the EU budget (to which all losses will first be debited) is joint-and-several, meaning that any one member state might have to pay the entirety. Financial markets interpret this, for example regarding the EU bonds being issued to finance the NextGenerationEU coronavirus reponse fund, as “it all tracks back onto Germany”.

So, Brussels’ and HMT’s calculations should include:

1. undrawn amounts within in-scope programmes and activities

2. programmes and activities committed in Q1 2021 under the carryover

But they cannot include:

1. programmes and activities that can be committed in Q2-4 2021 under the carryover

2. actual losses on these programmes and activities because they have end dates many years in the future

We do not know what the Maximum Possible Loss for the UK on all of this is (beyond that it would be 12% of the Maximum Possible Loss debited to the EU budget on account of this list of items). Indeed we cannot know it yet.

Nor are we told the likelihood of losses arising. It must be very high that some kind of loss will arise, in particular from the EIB’s loans outside the EU, and InvestEU. The EU has issued first-loss guarantees to the EIB/EIF for these programmes, and in turn the EIB/EIF are lending to poorly-rated non-EU sovereigns, or taking equity-level or subordinated debt positions in the underlying InvestEU transactions. That means they take the first or second loss in InvestEU transactions and will pass as much of any loss as they are able on to the EU, who passes 12% of that onto the UK.

The Maximum Possible Loss on all of that cannot be quantified before 31 March 2022, in the final list. It will be important to get sub-lists at that date from the EIB/EIF for all of:

1. EIB’s loans outside the EU

2. EIB’s InvestEU loans

3. EIF’s Invest EU guarantees and “equity commitments”

…and of course with all the transaction specifics so as to enable a calculation of the likelihood of losses.

This situation has been brought about by the loopholes in the treaty and the nature, size and duration of the liabilities that can slip through these loopholes: it is exactly what I wrote up in the CapX piece published on 14th July 2021.

The ongoing rumblings between HM Treasury and the EU feel very much like an orchestrated attempt to focus attention on what is quite a small difference in the overall scheme of things, and away from the much more serious deficiencies in the underlying agreement from a UK perspective.